Hi. Besides my normal work, I occasionally write about the economy and markets for Wealthsimple Magazine and its newsletter, TLDR, where I edit. You can read two such pieces below. The first, from 2026, is about oil; the second, from 2023, is about stocks. Others pieces are here and here. —Jared

Three Charts Explain Why War in Iran Hasn’t Cratered Stocks — Yet

March 9, 2026

Iran’s unprecedented move last week to close the Strait of Hormuz, a key shipping route for 20% of the world’s oil and gas, prompted the biggest sell-offs in several Asian and European stock markets since “Liberation Day” last April. But the rising risks of an energy shock (to say nothing of a widening regional war) didn’t trigger a full-blown market rout like you might expect. U.S. stocks ended the week down just 1.3%, while the TSX sank by 3.6%. Not great! But the S&P is still up 20% since this time a year ago and the TSX is north 35%.

So how come U.S. and Canadian investors, in particular, remained so calm last week? We found three charts that point to an answer.

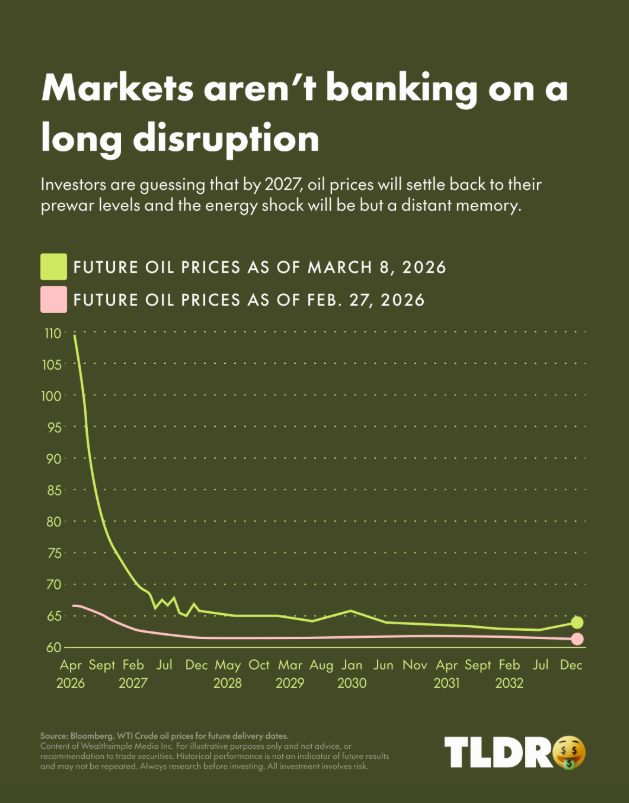

During the 1973 Oil Embargo, prices surged nearly 211% over six months, sparking a crippling global recession. But this isn’t the early ’70s or, for that matter, the early aughts, when crude prices rose by 628% over five years. As the Financial Times explained, shipping routes and pipelines have reduced global reliance on the Strait of Hormuz, and countries like the U.S. and China can lean on their strategic reserves. As of late Sunday night (when we finally gave up and went to sleep), crude oil had surpassed $115/barrel — a 72% jump since the war in Iran started. That’s dramatic! But it’s not economy-crushing (at least not yet).

There’s no denying that things are uncertain right now. But if you look at a wonky metric called the oil futures curve — which reflects what traders are betting oil prices will be in the future and what some big consumers, like airlines, are actually paying to lock in future supply — it shows that investors still believe, quite strongly, that supply will come back to normal within a year and the impact of recent disruptions will be limited. Why? U.S.’s and Israel’s operational success (so far) and a U.S. pledge to insure and escort tankers through the Strait of Hormuz. This optimism helps to explain why other sectors, especially U.S. stocks, have held fairly stable to this point.

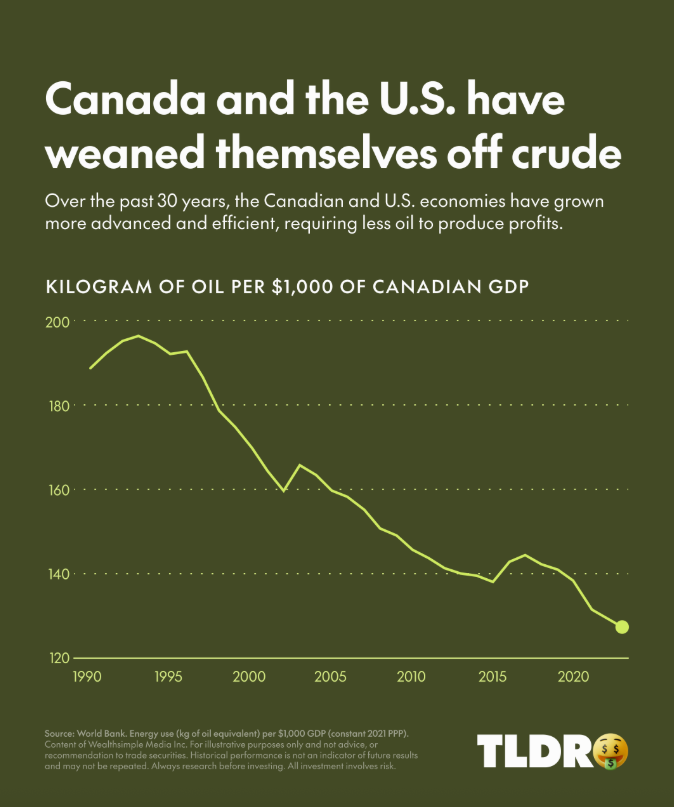

Oil remains Canada’s largest export — by far — but we use far less of it ourselves to spur business activity than we did three decades ago. That’s primarily because (1) vehicles and machines are more efficient, (2) natural gas and renewables have scaled up, and (3) we have a lot more service-oriented jobs that don’t require as much energy as, say, manufacturing. The U.S., our top trading partner, is even more energy efficient than we are, helping to insulate our interlinked economies from oil shocks. In fact we’re both now net energy exporters, meaning we produce so much domestically that we have extra to sell abroad — an advantage that most of our Asian and European allies lack.

Now allow us to hedge everything we just said

All of this explains why markets didn’t tank last week. But the longer this war drags on, the more likely it is we see oil prices continue to climb. Those numbers are already getting lots of headlines. But it’s worth bearing in mind that Canada and the U.S. are far better positioned than most to withstand an energy jolt.

—Jared Sullivan

2023: The Year of FOMM (Fear of Making Money)

July 2023

If you can remember anything about January of this year, it’s probably that everything felt bad. Interest rates were up. Recession alarm bells were blaring. Succession was ending soon. And pros like Mike Wilson, Morgan Stanley’s chief investment officer, were going around predicting that the stock market might drop another 20% in 2023. And that was after the S&P 500 and TSX had just nosedived by 19% and 8.5%, respectively, in 2022. The economic situation felt so grim that Wall Street’s yearly outlook, as tracked by Bloomberg, was the bleakest it had been in almost a quarter of a century. Investors felt more chipper after the dot-com bust, 9/11, and the ’08 financial crisis.

The backdrop to all this sourness was that the markets had just endured a dizzying few years. Between mid-February and late March 2020, the S&P 500 spiraled down by more than 30% as COVID swept the world. And on the heels of this downturn followed a frothy, stimulus-fueled rally (remember the $GME frenzy?) that sent the S&P up by more than 100% by November 2021. Was the whiplash over? Of course not. That rally met an abrupt, painful end in late 2021, when central bankers vowed to raise economy-slowing interest rates to control soaring inflation. Which a lot of folks assumed would crush the economy.

But that, to the shock of many, isn’t what happened. Yes, stocks fell sharply in 2022, costing individual traders some US$350 billion. But as interest rates rose in 2023, the labour market held strong. Corporate earnings came in far better than anticipated. AI sparked tons of optimism about the future. And, most important and surprising of all, inflation fell sharply without the economy skidding into a recession. At least, it hasn’t yet.

As the economic sky cleared, institutional investors, ecstatic with relief, plowed money back into markets, pushing up stocks globally by about 13% since January 1st of this year and kicking off a new rally. The tech-heavy Nasdaq has soared by an even more impressive 32%. (The light-on-tech TSX, up by only 4% YTD, is something of an outlier.)

But, as pros piled into stocks, many individual investors — average folks like you and me — refused to uncover their eyes and see that things looked … good. DIY trading activity was anemic throughout the spring and early summer. These so-called retail investors didn’t have FOMO, or fear of missing out. They feared, so they missed out.

So: why? Why did DIY investors sit out the rally? Bad vibes. That’s the most obvious answer. This rally just feels different, especially compared to the frothy one of 2021. And inflation bears most of the blame. Millennials and Gen Xers had heard Boomers talk about how terrible those ’70s price spikes were. But hearing about inflation and experiencing it are different things. We learned that it’s hard to feel optimistic about anything, really, if your paycheque isn’t keeping up with rising prices or if rate hikes might force you to sell your home.

Amplifying people’s discomfort, the economy had just gone through a huge adjustment, with millions of people being fired and rehired during COVID. Bad vibes on top of bad vibes. The next shoe was going to drop at any moment. You could feel it. So people stopped investing. According to IFIC data, Canadians bought $7 billion in mutual funds from January through May of last year. But, over the same period this year, they sold $9 billion worth of mutual funds — a $16 billion swing.

Here’s the wrinkle in the story: the reasons why DIY investors missed or were late to the spring rally were novel, but that they failed to capitalize on it was not. Retail traders, spooked by brisk declines in their portfolios, often sell off their assets at the bottom of the market and remain on the sidelines as stocks climb back up. They did that very thing in 2001, 2008, and 2020. And it cost them. The S&P 500 has tended to fall by 41% during bear markets, according to a recent paper, while it has typically risen by 162% during bull markets. Which helps to explain why families tend to lose more money panic selling during downturns than if they’d stayed invested: they often delay reinvesting and miss rallies.

So, if you’re wondering: OK, what now? Is the rally running out of juice, or is it just getting started? No one knows. No one ever knows. That’s sort of the point of this entire essay. Inflation surprised investors this year. Next time, it’ll be something else. To avoid making a costly blunder, successful long-term investors — Warren Buffett being the most famous among them — advise staying in the market and steadily investing through good times and terrible ones. Because boring, steady, diversified investing usually wins in the end. This year only reinforced the point: stay the course when bad vibes abound — and they will abound sooner or later — and don’t look away when other investors avert their eyes.